A Summary of the Key Items Released in Last Night’s Federal Budget

Treasurer Jim Chalmers has handed down the Labour Government’s Fourth Budget on 25 March 2025. The underlying cash balance will improve by a cumulative $207 billion over the seven years to 2028–29, compared to the 2022 Pre-election Economic and Fiscal Outlook. After delivering the first back-to-back surplus budget in nearly two decades, the forecast budget deficit for the current year is $27.6 billion, followed by a budget deficit for the next four years being $42.1 billion in 2025-26; $35.7 billion in 2026-27 $37.2 billion in 2027-28 and $36.9 billion in 2028-29.

This budget was said to ease cost of living relief and provide greater support for Australians, as inflation is now back within the Reserve Bank’s target band. The economy’s real GDP (inflation adjusted) is now forecast to be 1.5% in the current year; 2.25% in 2025-26; 2.5% in 2026-27,2.75% in both 2027-28 and 2028-29.

The unemployment rate is projected to remain low by historical standards at 4.25% in the current year and remains at 4.25% in the next four years through to 2028-29. Wages growth is forecast to be 3.25% in2025-26 and in 2026-27; 3.5% in 2027-28 and 3.75% in 2028-29.

Gross federal government debt is forecast for the 2025-26year at $1,022 billion (35.5% of GDP) and will increase over the following three years - $1,092 billion (36.5% of GDP) in 2026-27; $1,161 billion (36.9%of GDP) in 2027-28; $1,223 billion (36.8% of GDP) in 2028-29.

It is important to note that this is a pre-election budget. The Opposition Leader is scheduled to deliver his budget reply on Thursday, most likely being the last sitting day of Parliament. With the federal election due on or before 17 May 2025, it is crucial to understand that the measures announced in this budget will only be introduced into Parliament by a newly elected government, whichever party that may be.

A selection of the budget announcements follow.

Personal Income Tax Rates

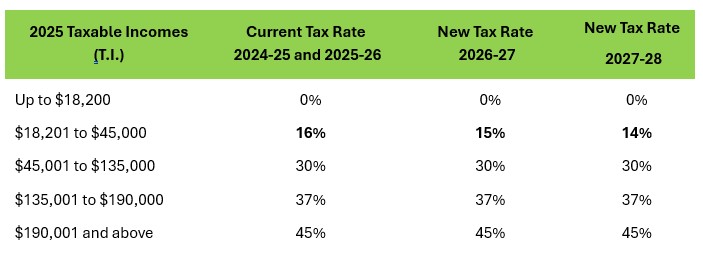

The Government will introduce a new round of tax cuts for all Australian taxpayers, commencing 1 July 2026. These measures are aimed at providing continued cost-of-living relief. The changes include:

- From 1 July 2027, the 15% tax rate will be further reduced to 14%.

- From 1 July 2026, the 16% tax rate will be reduced to 15%.

This new round of tax cuts is in addition to the initial stage of tax cuts legislated by the Government last year, which have been in effect since 1 July 2024. The new tax rates are as follows:

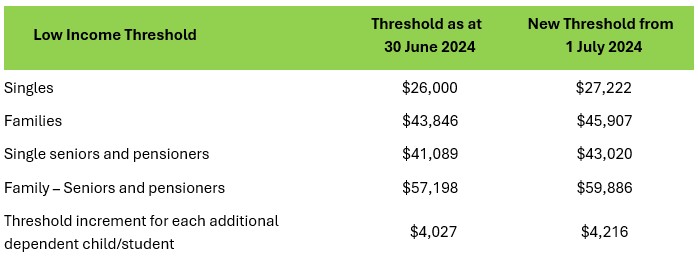

Increasing Medicare Levy Low-Income Thresholds

The Government will increase the Medicare levy low‑income thresholds for singles, families, and seniors and pensioners from 1 July 2024 to provide cost‑of‑living relief.

The Medicare Levy itself will remain at 2%.

Energy Bill Relief

The Government has announced the continuation of its energy bill relief program which was due to expire on 30 June 2025. The initiative will be extended for an additional two quarters, providing households with two further $75 energy bill rebates through to 31 December 2025.

This extension aims to help ease cost-of-living pressure and support Australians in managing their household energy expenses.

Two-Year Ban on Foreign Ownership of Established Housing

To support housing availability for Australian residents, the Government will introduce a two-year ban on the purchase of established dwellings by foreign persons, including temporary residents, effective from 1April 2025.

To ensure effective enforcement of this measure, the ATO will receive funding to monitor compliance and implement the ban.

Help to Buy Scheme Expansion

The Help to Buy Scheme is a shared equity scheme where the government co-purchases a home with eligible buyers. It is a low deposit scheme, requiring a 2% deposit, while the government funds up to 30% for existing properties and up to 40% for new homes.

The Government has announced it will increase its equity investment in the Help to Buy scheme by an additional $800 million, taking the balance to $6.3 billion.

In addition, the income caps for eligibility have also been increased from $90,000 to $100,000 for individuals, and from $120,000 to$160,000 for joint applicants and single parents.

The property price caps will also be increased and linked with the average house price in each State and Territory. For example, the new property price cap for New South Wales -capital city and regional centres is now $1,300,000.

Applications will open later in the year, once all necessary updates have been made.

Higher Education Loan Program (HELP) Debt – 20% Reduction

The Government will introduce a one-time 20% reduction on the outstanding balances of all HELP debts and other income-contingent student loans, and has announced changes to the repayment system, ensuring that repayments increase progressively with income. This reform will raise the minimum repayment threshold and will index the threshold to growth in average earnings.

This new measure will have effect from 1 July 2025.

Final Stage of Superannuation Guarantee Rate Increase

From1 July 2025, all employees will benefit from the final stage of the legislated increase to the minimum superannuation guarantee (SG) rate. The SG rate will increase from 11.5% to 12%. This change marks the completion of the phased increase to the SG rate.

Small Business and Franchisee Support and Protection

The Government will provide $7.1 million over two years from1 July 2025 to the Australian Competition and Consumer Commission to strengthen regulatory oversight of the Franchising Code of Conduct.

A further $0.8 million will be provided to Treasury to develop and consult on options to extend protections against unfair trading practices to small businesses and protect business regulated by the Franchising Code of Conduct from unfair contract terms and unfair trading practices.

Banon Non-Compete Clauses

The Government has announced it intends to ban all non-compete clauses for workers earning less than the high-income threshold in the Fair Work Act – currently $175,000.

In tandem with this change, the Government is also looking to close loopholes that currently allow businesses to engage in non-competitive practices such as fixing wages and no-poach agreements.

These changes will allow workers to move more freely between employers or to start their own businesses.

The Government will engage in consultation, with changes expected to take effect from 2027.

Amendments to Existing Measures – Managed Investment Trusts

The Government will amend the tax laws to provide greater clarity around the eligibility requirements for concessional withholding tax rates applied to managed investment trusts (MITs). These changes ensure that only legitimate investors can continue to access concessional withholding tax rates in Australia complementing the ATO’s strengthened guidelines aimed at preventing misuse and avoidance through inappropriate arrangements.

This measure will apply to fund payments from 13 March2025.

Apprenticeship Announcement Changes

The Government has announced its plans to extend the current Australian Apprenticeship Training Support Payment and Priority Hiring Incentive by six months until 31 December 2025 while they consider longer term reforms and undertake consultation with stakeholders.

The Government has also announced it will increase Living-Away-From-Home Allowances for apprentices that travel to take up an apprenticeship and also increase the level of Disability Wage Support payments to employers.

They also announced in January 2025 the inclusion of residential construction apprenticeships as part of the Key Apprentice Program, and from 1 July 2025 paying eligible apprentices $10,000 in incentive payments over the course of their apprenticeships.

Enhancing Tax Practitioner Regulation and Compliance

The Government will enhance the regulatory powers of the Tax Practitioners Board (TPB) by strengthening available sanctions, modernising the tax practitioner registration framework, and providing additional funding to the TPB to undertake additional compliance targeting high-risk tax practitioners over four years from 1 July 2025.

This measure will protect taxpayers from tax agent misconduct, including poor and unlawful tax advice, and maintain community confidence in the integrity of the tax system. In addition, the measures will support the long-term sustainability of the tax profession by streamlining there-entry process for tax agents and BAS agents returning to the profession after a career break.

This measure will have effect from 1 July2025.

Deferral of Proposed Changes to Foreign Resident Capital Gains Tax

The Government will defer the commencement date for the previously announced measure to broaden the scope of capital gains tax (CGT)for foreign residents, originally announced in the 2024/25 Budget.

Instead of commencing on 1 July 2025, the measure will now take effect from the later of:

- 1 October 2025, or

- The 1 January, 1 April, 1 July, or 1 October following the date the legislation receives Royal Assent.

Details of the previously announced measure include:

-

- clarifying and broadening the types of assets that foreign residents are subject to CGT on;

- amending the point-in-time principal asset test to a 365-day testing period; and

- requiring foreign residents disposing of shares and other membership interests exceeding $20 million in value to notify the ATO prior to the transaction being executed.

Deferral of Start Date for The Clean Building MIT Withholding Tax Concession

The Government will defer the commencement date for the previously announced measure on the extension of the clean building managed investment trust (MIT) withholding tax concession to include data centres and warehouses that meet specified energy efficiency standards.

The revised start date will be the first 1 January, 1 April,1 July, or 1 October following the date the legislation receives Royal Assent.

Strengthening Tax Integrity

The Government will provide $999m over four years to extend and expand tax compliance activities. Key components of this funding include:

- $717.8million over four years from 1 July 2025 for a two-year expansion and a one-year extension of the Tax Avoidance Taskforce. This funding will enable the ATO to scrutinise multinationals and large taxpayers.

- $155.5million over four years from 1 July 2025 to extend and expand the Shadow Economy Compliance Program to target non-compliant economic activities such as worker exploitation, under-reporting of income, illicit tobacco, and other shadow economy activity that enables non‑compliant businesses to gain an unfair advantage.

- The Personal Income Tax Compliance Program will receive $75.7 million in additional funding over four years, commencing 1 July 2025. This funding will support a strategic mix of proactive, preventative, and corrective compliance activities, targeting key areas of individual taxpayer non-compliance to ensure the integrity of the tax system is maintained.

Restricting Foreign Ownership of Housing

Aspart of the Government’s broader strategy to increase housing supply across Australia, new restrictions will be introduced to prohibit foreign persons from purchasing established dwellings, unless specific exceptions apply. Exceptions include:

- Investments that materially increase the overall housing supply or support housing availability at a commercial scale, and

- Purchases by foreign-owned companies for the purpose of providing accommodation for workers in certain circumstances.

To support the enforcement of these measures, the ATO and the Treasury will receive targeted funding, including:

- $5.7million over four years from 2025–26 to enforce the ban on foreign ownership of established dwellings, and

- $8.9million over four years from 2025–26, plus $1.9 million annually from 2029–30,to implement an audit program and strengthen compliance activities, particularly in relation to land banking by foreign investors.

%20(2).jpg)